The D&G Central London Index - Q4 2017

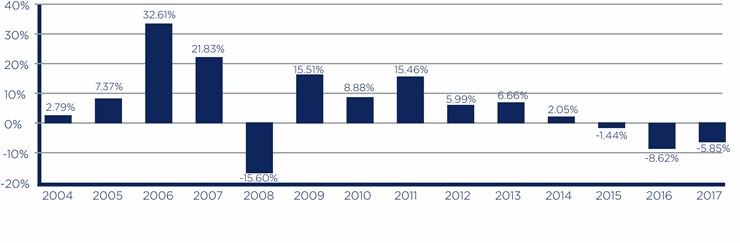

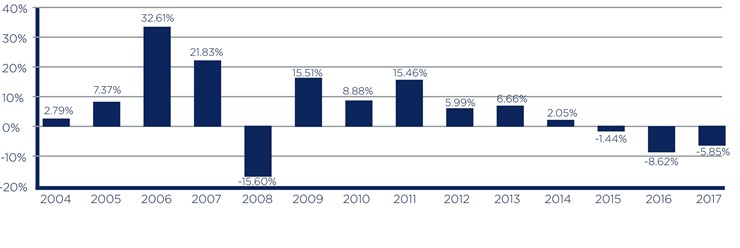

Q4 2017 - values stabilise

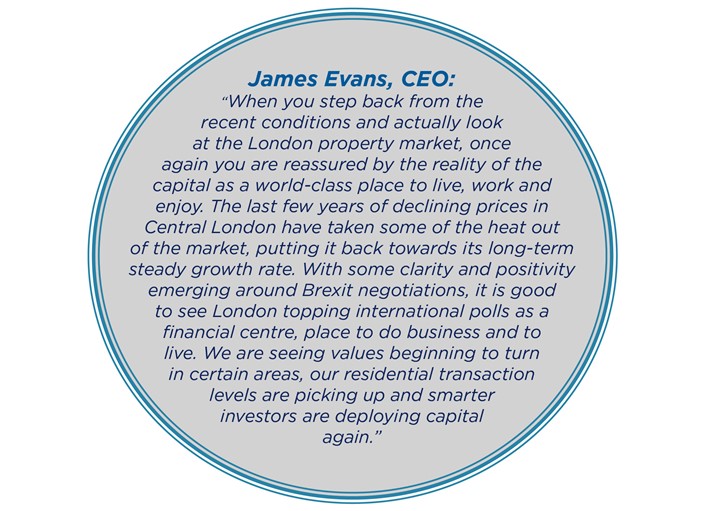

In the final quarter of what has been a difficult year, the themes of Brexit uncertainty and a botched General Election carried through – although at the end of the quarter we saw some degree of political agreement with Europe and a shift towards more positive post-Brexit scenario reporting.

The budget delivered some good news to first time buyers with the reduction of Stamp Duty on sub £500k properties (0% on sub £300k), and with low forecasted GDP growth, the future of low interest rates and historically very cheap money looks here to stay.

Furthermore, with a degree of nervousness around the historic high levels of stock markets, and three and a half years of falling Central London property prices, investor sentiment is beginning to return: the early stage of a reverse ripple effect is seeing money come back to central London, and its solid yields, particularly in Emerging Prime. Whilst we are seeing a small decline to the Emerging Prime market, our data tells us that Prime has bottomed out.

2018: the year of the Reverse Ripple? Are we reaching peak uncertainty-fatigue and is Central London confidence rallying?

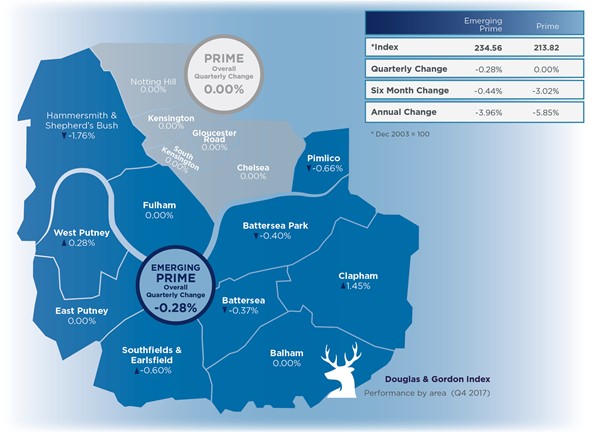

Emerging Prime Highlights

Sales

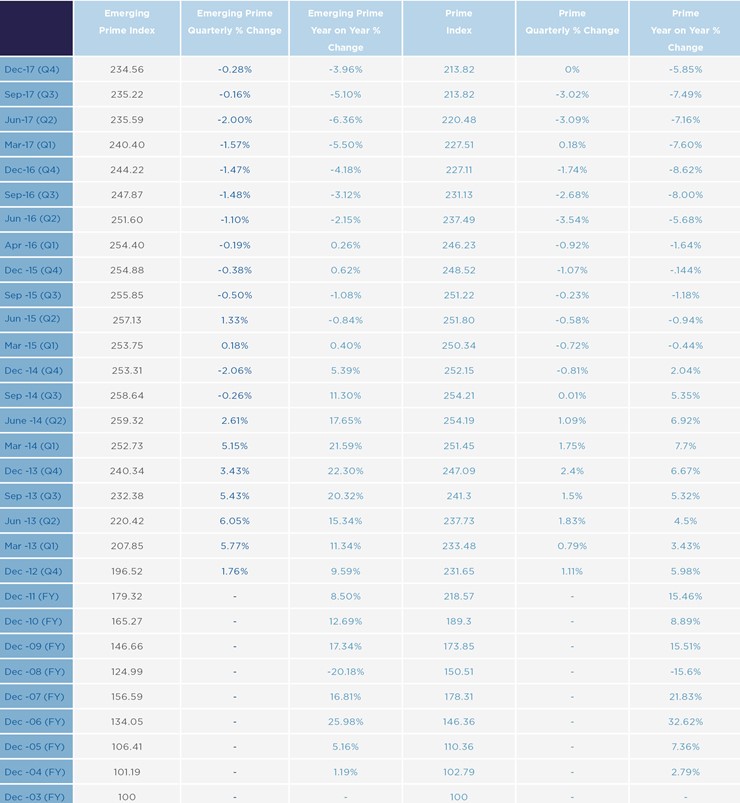

Prices weaker (- 0.28%) in Q4 than Prime, although Emerging Prime performed better that Prime in 2017, and many areas saw little change on Q3.

There is evidence that the top end of the house market (5 Bed) is slightly firmer in Clapham South and West Putney.

We have noted that the cut in SDLT for first time buyers has already helped in Clapham South, and enlivened a hitherto subdued Flat market

We continue to note that in some areas the differential between flats and small houses is eroding (Balham, Battersea Park).

There is a general absence of Buy-To-Let investors, owing to the double-whammy of SDLT levy and the tapered withdrawal of tax relief; but just as in Prime, we have noted some “strategic” investors are starting to look.

Lettings

The seasonal impact of Q4 meant that houses were slightly weaker in Battersea Park, Fulham, Hammersmith and Pimlico – but stronger in Putney, where corporate relocation agents are active.

Price reductions remain a theme – there is a general realisation from landlords that the rental market remains tough.

Landlords have adjusted expectations around price reductions and levels of occupancy have risen.

As Battersea Power Station nears completion, our view is that demand for rental property will grow substantially.

Prime Highlights

Sales

Q4 2017 values were flat - our valuers felt that the falls in Q2 and Q3 have now fully played out.

The D&G Prime index is –15.89% from its peak in September 2014. In the last bear market, the index fell -17.80% between December 2007 and April 2009 during the depths of the banking crisis, more evidence that we have reached the bottom of the correction.

£ Sterling remains attractive to foreign buyers – and we have seen more substantial interest in London from investors and developers.

Lettings

Quality stock is renting well, and those landlords with well-presented properties are reaping the benefit.

Kensington 2 bed flats are slightly up, while Chelsea and Westbourne Grove houses are slightly weaker, owing in part to seasonality.

Despite a challenging market over the last two years, many of our landlords have benefitted from an RPI uplift, a major feature of investing in this asset class.

Looking Ahead

So, to forecasts: obviously there is much negotiation still to navigate during the UK’s transition through Brexit. But whilst the doom-mongers views are well-publicised, it is interesting to note an increase in recent news stories that remind us of the desirability of London as a place to work, live and play.

First, that London remains a major destination for Ultra High Net Worth individuals - Wealth-X, a firm that does research on ultra-high net worth (UNHW) individuals, has looked at the regions in which the most people with a net worth of $30m upwards opt to live. New York came top, with an UHNW population of 14,574 people. Of these, 8,340 are residents and 6,234 are second home owners. London was second, with an UHNW population of 9,301, followed by Los Angeles (8,272), Hong Kong (8,009) and Singapore (7,953). (Source: Independent Newspaper 09/12/2017).

Second, Britain’s business climate remains attractive. The U.K. ranks first for the first time in Forbes’ 12th annual survey of the Best Countries for Business, where 153 nations are rated across 15 different factors, from property rights, taxes, technology and innovation to freedom, corruption, red tape and investor protection.

Indeed, Wells Fargo, Facebook and Apple have made major long-term investments into London since the Brexit vote, with a new European headquarters, a new home for 9,000 employees and a campus in 2021 respectively.

Lastly, London is still ranked as the world’s top financial centre. The Z/Yen Global Financial Centres Index, which is published every six months, scores cities out of a total 1,000 points and lists London as number one with 780 points. New York is second with 756 points, and Hong Kong (744) has usurped Singapore to take third place in the latest ranking. Paris and Dublin, the two cities that have positioned themselves to host financial services firms looking to relocate from post-Brexit Britain, are positioned a distant 26th and 30th, respectively.

All this points to evidence that the rest of the world is taking the long-term view and backing London as strongly as ever.

About Douglas & Gordon

- Douglas & Gordon was founded in Chelsea in 1958 and remains independently owned.

- The company employs over 200 people in 19 areas across central, west, southwest and north London, property services.

- Services include: Residential sales, lettings & developments; Property management; Corporate services; Professional valuations; Refurbishment & interior services, Asset Management; Block Management.

- £10bn residential property under management.

Our Data

The D&G Emerging Prime Index was established in 2014 using our proprietary data stretching back to December 2003.

The index is valuation based and covers the following areas of London: Battersea Park, Battersea, Balham, Clapham, East Putney, West Putney, Southfields & Earlsfield, Hammersmith, Shepherd’s Bush, Pimlico & Westminster and Fulham.