The D&G Central London Index - Q3 2018

The Chancellor delivered some cautiously optimistic news on the UK economy, despite the headwinds of Brexit, upgrading the growth forecast from +1.3% to +1.6% with successive rises beyond that for the next few years.

Improved tax receipts and low interest rates have enabled increases in the personal income tax allowance as well as injections of cash into the NHS, defence, social security, transport and housing.

There were no nasty surprises, and indeed the government has pledged to continue the Help to Buy scheme for another five years. This, together with the axing of SDLT for all first-time buyers of shared ownership properties valued up to £500k, has helped stimulate the first time buyer market, particularly with newly built homes.

In our view, the government has been myopic in its treatment of private landlords, particularly with regards to the changes in stamp duty for the purchase of second properties, and some are definitely selling up. This is constraining supply, so demand from tenants increases, thus rents rise.

There was little joy for landlords in this budget and with the tax break on mortgage interest on Buy-to-Let properties still tapering away, and Lettings relief now limited to properties where the owner is in shared occupancy with the tenant, it has never been more important to get good expert guidance from your agent on how to maximise your investments.

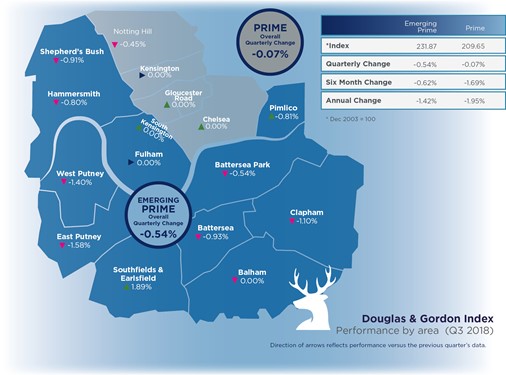

Looking at our recent round of London property value indices, we’re definitely seeing a tapering off of the falls in prices that have been a feature of the market for the last four years. Rental values are holding firm in most areas, with the emerging prime index showing an increase of +0.57% on the last strong quarter.

In fact, looking beyond the averages and drilling into the data further, we are seeing sale prices rising again for certain types of property and specific areas, particularly at the top end.

Our own business data also shows a large rise in people registering interest in buying property, in a market where people are not moving as quickly as in the past. There is definitely pent up demand brewing, and our view is that once the Brexit deadline has happened in March we could well be in for a surge in values again, mimicking the pattern of previous cycles.

As equity markets come off the boil after one of the longest bull runs in history, trade wars loom, European countries face their own challenges (German leadership, Italian banks, Greek debt, French reform, etc.), so the UK, and London property specifically, looks attractive, despite the Brexit shadow.

London is unparalleled on the global stage as a desirable place to work, rest and play. Witness the continued investment into major developments like Battersea, Nine Elms and Croydon. Or Unilever deciding not to relocate its HQ to the Netherlands, and other financial institutions confirming that they will not be down-weighting their London presence after all.

London’s stability, diversity and vibrancy, let alone the calibre of its academic, cultural, legal and commercial institutions, will continue to endure for generations to come.

Emerging Prime Highlights

Rental Value Performance - D&G Emerging Prime

Lettings

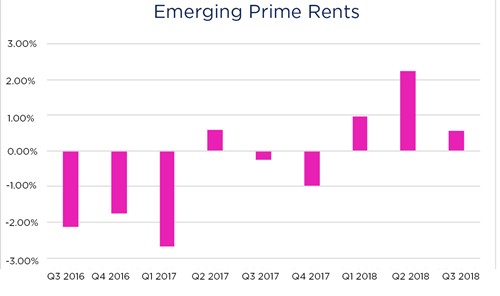

- Rental values were firmer in Q3 2018: +0.57%

- This figure comes during a traditionally weaker quarter and after a particularly strong Q2 (+2.23%)

- A major factor is people sitting tight for longer before buying, continuing to rent

- Many of our offices reported strong renewals

- Yields looking particularly good in some areas

- Legislative changes for BTL investors, taxation changes, and some landlords deciding to sell-up will impact supply of rental properties with a knock-on effect driving up rental values.

Sales

- In Q3 2018 the index was -0.54%, remaining weak after a soft Q2

- Price weakness overall was in the smaller flats and smaller house market in some postcodes

- Larger family houses were stable (4 bed houses seeing a rise in value)

- Yields are looking attractive 4.5% to 5% in some areas for investors

- Fulham, Southfields & Earlsfield all saw some rises in performance versus the previous period

Prime Highlights

Rental Value Performance - D&G Prime

Lettings

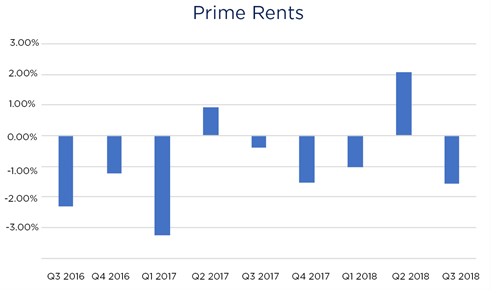

- Prime Rental index in Q3 2018 down: -1.58%

- The rental market is seasonal and Q3 2018 followed a strong Q2.

- Rental values were mainly stable but the overall number was pulled down by weakness in the smaller house market and peripheral areas of Prime, masking some rises in value in certain areas

- With the Sales market subdued many potential buyers continue to rent and many tenants looking for longer tenancies than in the past

Sales

- In Q3 2018 the index was -0.07%, pulled down by weakness at the bottom end of the market in the peripheral areas of Prime.

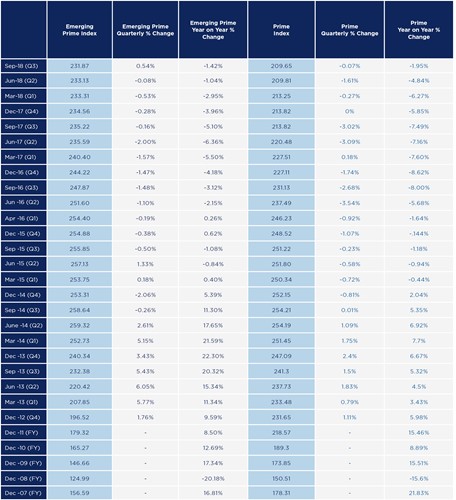

- The D&G Prime Index is -17.53% from its peak in September 2014 (It fell -17.80% between December 2007 and April 2009)

- Prices of larger properties remained stable, and have enjoyed a better 12 months than smaller flats

- Political uncertainty and SDLT levels have continued to have a dampening effect on transaction volumes

- Chelsea, South Kensington, Kensington and Pimlico all saw rises in performance

About Douglas & Gordon

- Douglas & Gordon was founded in Chelsea in 1958 and remains independently owned.

- The company employs over 200 people in 19 areas across Central, West, South West and North London, property services.

- Services include: Residential Sales, Lettings & Developments; Property Management; Corporate Services; Professional Valuations; Refurbishment & Interior Services, Asset Management; Block Management.

- £10bn residential property under management.

Our Data

The D&G Emerging Prime Index was established in 2014 using our proprietary data stretching back to December 2003.

The index is valuation based and covers the following areas of London: Battersea Park, Battersea, Balham, Clapham, East Putney, West Putney, Southfields & Earlsfield, Hammersmith, Shepherd’s Bush, Pimlico & Westminster and Fulham.