The D&G Central London Index - Q2 2018

Q2 2018 Market Review and outlook - Sales index shows values under some pressure, whilst Rental index performs strongly.

“The only constant in life is change”. A saying coined by Heraclitus, the ancient Greek philosopher in 501 BC, and as true of property markets as it is everything else.

Central London is now technically in the 16th quarter of a bear market, with sales transactions in some areas widely reported down by 20% over the last three years according to Land Registry figures.

The National Association of Estate Agents, looking at offers that have been accepted, says that 86% of sales among its members went for less than the asking price last month.

At D&G, however, we are witnessing a significant rise in prospective buyers and tenants compared to this time last year. All our offices are reporting 20-30% more applicants, and overall we have just enjoyed a 65% uplift year-on-year in terms of customers coming to us to transact.

An increase in above-asking-price sales and sealed bids across our network is perhaps indicative of the mood changing for the better.

It is certainly a buyer’s market, but for how much longer? The secret of course to a successful sale is smart valuing, thorough understanding of the motivations of both seller and buyer, sensitive price management and negotiation with a diligent agent taking the lead on all aspects of the transaction, actively finding the right buyers and guiding customers through to completion.

There is good news for landlords: our index shows a significant rise in rental values across all our areas, in fact the best quarter for many years. And whilst we have been selling some rental properties for our landlords who have inevitably felt the pressures of the reduction in tax advantages on rental income, we have also been assisting long term investors with bulk purchases of investment properties, increasingly new builds, given the improvement in yields in some areas of London.

In this climate, as ever, the key for landlords is to focus on quality and cost management; we have been helping customers with regular reviews of buy-to-let mortgage rates, finding and keeping good tenants, and maintaining and improving properties to a high standard, as well as assisting with lease extensions, freehold purchasing and insurance arrangements.

So much of what drives a property transaction is at a highly local level, but obviously macroeconomic events have their effect. Sterling has weakened against the Dollar again, presenting double discount opportunities for foreign buyers and investors.

The Bank of England kept interest rates on hold again, despite increasing speculation they were going to rise. Of course, in time, they will rise, but only by small increments of 25 basis points at a time, and remember that they are still at low historical levels: money is cheap to borrow and easily lent.

Brexit uncertainty has added some volatility into matters, but at least clarity can only increase over the next six months. Mostly shrugged off by markets and individuals, with some exception around long term planning, e.g. foreign bank employees being repatriated, which we think is unlikely to happen at scale. In the short term, it has bolstered the rental market as people choose to rent for longer.

SDLT continues to act as a brake on transaction volumes, and our view remains that changes to this tax under George Osborne’s tenure as Chancellor of the Exchequer, have been ill-conceived and broadly damaging despite the more positive changes made in the last budget for first time buyers. Perhaps there is hope that should the Government want to re-stimulate the market post Brexit in Q2 next year, they will look on this as a powerful lever to pull, redressing previous errors?

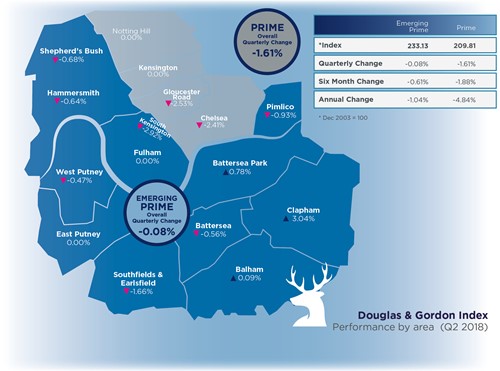

Emerging Prime Highlights

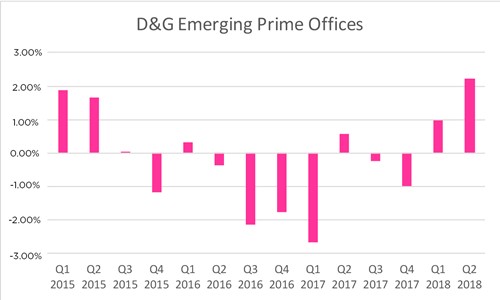

Rental Value Performance - D&G Emerging Prime

LETTINGS

• Rental values in Q2 2018 were firmer: +2.23%.

• Seasonal factors aside, this was an exceptionally strong quarter.

• This is partly as a consequence of the suppressed sales market, with people continuing to rent for longer.

• There has been an uptick in Landlords selling off some property, e.g. those for whom the changes in taxation has narrowed the profitability of their rentals, which reduces supply and boosts demand amongst tenants.

SALES

• Q2 2018 Index was -1.12%, a reversal after a positive performance in Q1.

• Price weakness was in the flats market, driving this decline, with the exception of Clapham and Battersea Park which posted gains of +3% and +0.78% respectively.

• Of course declines in prices ultimately increases affordability, which in turn re-stimulates the market further down the line.

• Similarly, yields are now looking attractive in some areas for investors.

Prime Highlights

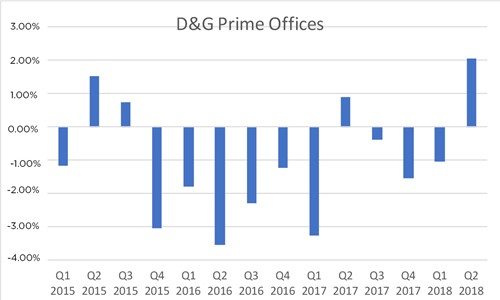

Rental Value Performance - D&G Prime

LETTINGS

• Q2 Prime Rental Index up +2.07%.

• Whilst this time of the year is normally the strongest quarter of the year, this is a good figure, the best quarter for some years, especially given the period of protracted weakness.

• With challenges in the Sales market, many potential buyers are continuing to rent.

• Demand has risen: D&G currently have a +72.5% increase in applicants registered actively looking to rent versus this time last year.

SALES

• Q2 2018 Index was -1.61%, pulled down by weakness in the bottom end of the market.

• The Index is down -17.47% from its peak in September 2014. In the financial crisis between 2007 and 2009 the index fell – 17.80% before bouncing back strongly. By any measure this looks like the tail end of the bear market. Savvy buyers will run out of time to gain a long-term bargain.

• Quality properties sell in any market and can achieve a great price.

• Sales volumes are down compared to previous years but good prices are still being achieved and our stock level is up year on year.

D&G Performance Highlights

D&G No.1 out of 1067 agents across D&G Land for most properties Let between 1st April and 1st July and year-to-date, 2018 (Source: Zoopla).

In more signs that things may be changing, the supply of homes on the market in the UK fell overall in June but increased in London to its highest level for three years, latest research shows. New home sellers were up 2.8% in London in June compared with the previous month (source: PropertyWire 4th July 2018) and the latest RICS Residential Market Survey report for June shows 10% more surveyors reporting an increase rather than a decrease in instructions, becoming the first time since early 2016 that this figure has been positive for two consecutive months.

Yet again, Britain has retained its place as the top European destination for foreign investment. According to the EY Attractiveness Report, there was a 22% increase in digital investment into the UK. London continues to be a global financial and tech centre and with the development of Battersea Power Station and King’s Cross attracting the head offices of Apple, Facebook, and Google as well as American financial giant Wells Fargo committing to London with its new HQ building in the City.

Thoughts from a first-time buyer

First time buyers are the lifeblood of the property market. They are also, by definition, a significant cohort of those who rent. We asked Alice, who graduated from Bristol University three years ago and now works and lives in South London, how she and her generation feel about the property market.

“For myself and many of the peers I associate with as a young, first-time buyer, financial morale is fragile at present.

That’s because we are, in many ways, worse off than the generation before us, thanks to the gap between property prices and incomes of millennials being at historically high levels. For many young people today, the property ladder is not a ladder where stability can easily be reached.

I have been renting in south London for three years, haven’t yet bought a home, and would be lying if I said I wasn’t anxious when I read today’s media. Yet, much of this coverage I believe to be filled with baseless assertions. In my view, my generation have every reason to be positive.

Firstly, I don’t see renting as a bad thing. In Germany, for example, renting has long been the norm. And, from talking with friends, I’ve come to realise that asset-rich baby-boomers advising us to buy property may not have clocked that we might not want that from life just yet, if at all.

Of course, putting off any financial decision comes at a price. But home ownership is an enormous responsibility which raises existential questions about relationships, work, raising families… The list goes on. For a mildly conflicted young person, there is a lot to be said for biding one’s time.

A significant positive is that if you’re ready to take the plunge and buy a home, lenders are beginning to meet us half way, there is active government support in the Help-to-Buy scheme and there have been major changes to stamp duty. If we choose where to invest wisely, it’s not all doom and gloom. We just need to find the right support network and to assess all of the options available to us.

Whatever happens, we mustn’t be scared by what we read in the headlines, as confidence is a key component in making the right financial decisions.

We are in charge of our own housing destiny, and that in itself is exciting.”

MoneySupermarket research shows that 19% of people are looking to put their savings towards home ownership. The analysis also found that the period between 1996 and 2016 saw a 54% increase in the number of 34- to 50-year-olds renting.

The problem of affordability can be resolved through a combination of elements: wage inflation, price correction, reduced SDLT rates, access to great mortgage deals, the Help-to-Buy scheme and for some lucky people – a helping hand. The bank of mum and dad is the gift that keeps on giving: Millennials are likely to inherit £1.2trn from their parents – an average of more than £230,000 each – during the next 30 years. Research by financial services group Sanlam found that 64% of those aged 25 to 45 expected some kind of assets or property inheritance.

D&G celebrated 60 years of trading this month. We have successfully weathered all sorts of market conditions over the last six decades, including the worst recession since the 1930s – the ”Credit Crunch”. Every time, the London market has shown just how robust it is over the long-term. We remain family-owned and independent, still focused on our customers, quality and delivering the best results for everyone.

Our thanks, as ever, to all our long-standing clients for the loyalty. Here’s to another 60 years of loving London!

About Douglas & Gordon

- Douglas & Gordon was founded in Chelsea in 1958 and remains independently owned.

- The company employs over 200 people in 19 areas across Central, West, South West and North London, property services.

- Services include: Residential Sales, Lettings & Developments; Property Management; Corporate Services; Professional Valuations; Refurbishment & Interior Services, Asset Management; Block Management.

- £10bn residential property under management.

Our Data

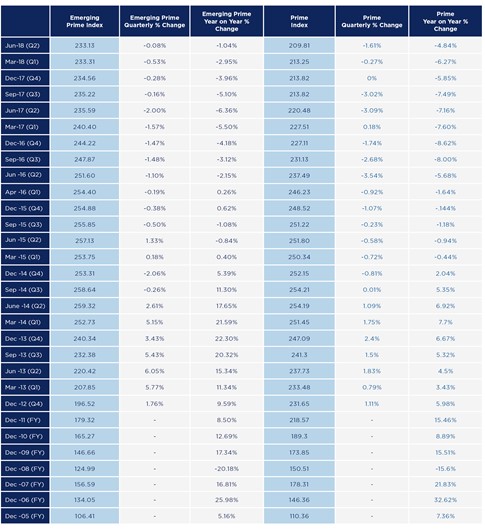

The D&G Emerging Prime Index was established in 2014 using our proprietary data stretching back to December 2003.

The index is valuation based and covers the following areas of London: Battersea Park, Battersea, Balham, Clapham, East Putney, West Putney, Southfields & Earlsfield, Hammersmith, Shepherd’s Bush, Pimlico & Westminster and Fulham.