The D&G Central London Index - Q1 2018

Q1 2018 - High levels of interest, lower transactions, stable prices and the return of the first time buyer.

Looking back across 20+ years of our own highly local London property price data, we get to see some useful patterns – not least that with every market correction comes a return to long-term growth. Our latest data continues the themes we reported previously: the downturn has played out for four years now, and so it is no surprise we are seeing an increase in value across certain properties in many of our areas, something that the media appear to have missed.

As uncertainty slowly clears from the political landscape and the economy continues to show its resilience, we believe that the historically low transaction levels will create pent-up momentum: people always need to move, always need to live and work as locally as possible, and many want to diversify their investments. Now with the market turning, in several areas, we are already seeing an uplift in interest, with applicant numbers across both rental and sales 20% up year on year. Recent research amongst our landlords shows that 34% are considering adding to their portfolios in 2018.

Furthermore, there are signs of a resurgence in first time buyers – the life blood of the market, with reports from some of our offices that the market around the £500,000 level has taken off post November’s budget and the positive move on SDLT rates.

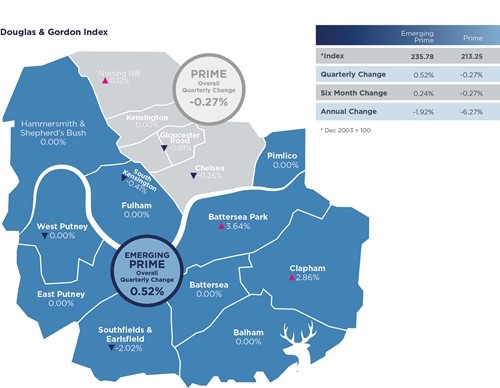

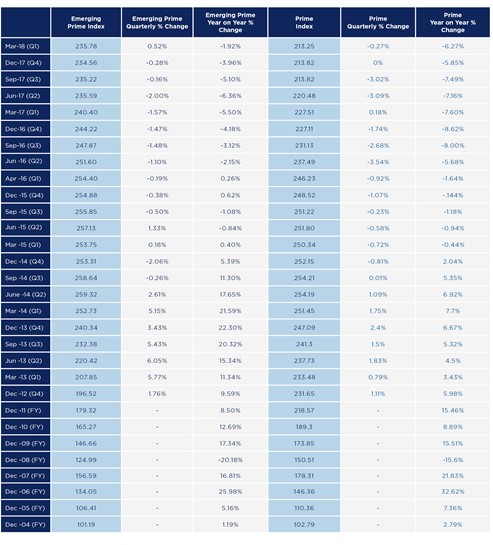

Emerging Prime Highlights

SALES

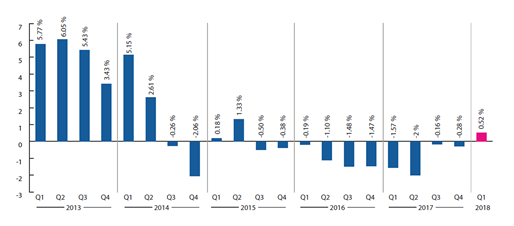

• The index was up +0.52%, from a previous quarter result of -0.28%, which is excellent news, with the rise driven in part by the performance of larger houses, particularly in Battersea and Clapham South.

• Applicant numbers are up 20% year on year, but not all committing properly to purchase, given the lower rate of exchange.

• Buy-to-let investors are not rushing back in, but we are seeing a few long term investors taking advantage of the historical discount in values and adding to their portfolios.

LETTINGS

• Rental values were firmer (+0.97%), due in part to a seasonal pick up.

• Battersea Park +1.88%, Clapham +2.31%, Fulham +1.07%, Pimlico +3.11%

• Houses were mixed, although managers are reporting that there remain some difficulties (e.g. reluctance of some landlords to accept sharers, despite them being fully-vetted professionals).

• From an investor perspective, good yields of c.4.5% are available in several areas of Emerging Prime, and as a whole rents have remained steady this quarter.

Prime Highlights

SALES

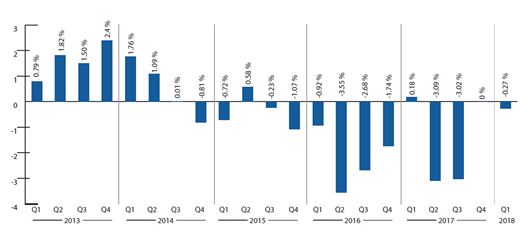

• In Q1 our index was down 0.27%, driven by weakness at the lower end of the market.

• SDLT a real break on transactions, which are at a historical low level.

• The differential between flats in Prime and Emerging Prime is eroding, as London’s dynamic culture and demographics move around.

LETTINGS

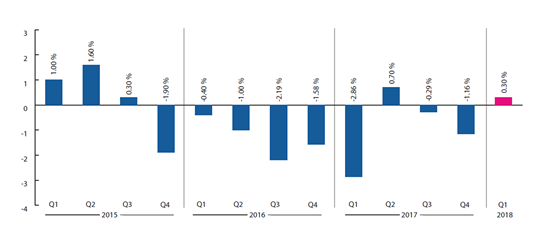

• The index is down -1.04% this quarter, and we are seeing a number of interesting trends emerging: when longer term tenancies are coming to an end now, landlords are having to reduce rents owing to the difference in market conditions a few years ago.

• Added to this, tenants are savvy and in anticipation of negotiating lower rents many are looking at alternative accommodation.

• The rise in quality of stock in areas outside Prime Central London is also having a downward pressure on rental values.

• There has been a high level of renewals, with people sitting tight and being guarded about buying.

• Chelsea and Notting Hill rents were up, +0.3% and +0.37% respectively.

Rental Market Themes

Summary

We believe now is a good time to take advantage of excellent pockets of value in London residential property. For landlords, whilst the sector is certainly under some policy strains, we are seeing yields hitting 4.5% in areas of Emerging Prime; and for those people looking to trade up into larger houses, then the detail of our indices shows that time is running out for getting a discount on a four bedroom house in Fulham, for example.

The government is increasingly looking to address the severe imbalance between low supply and high demand. Infrastructure is being invested in, e.g. the new tube line in Battersea, and Sajid Javid, the Housing Secretary, has indicated that new rules would allow some homeowners to add up to two storeys to their houses “The density of London is less than half that of Paris. We don’t want London to end up like Hong Kong…but it will be quite surprising how easy we want to make it for people who want to build upwards” (Source: FT).

Certainly SDLT continues to act as a handbrake on transaction numbers, particularly penalising the upper-mid and top end of the market, but we continue to see a steady flow of money into residential property in our areas owing in part to inheritance planning.

Furthermore, London is becoming an established technology centre, alongside its traditional financial, legal, cultural and educational powerhouse position. We’ve seen Battersea Power Station’s popularity (Apple), and Google and Facebook expanding their HQs. Now, US growth investor Motive Partners, which focuses on fintech projects, has chosen Canary Wharf for its new European hub.

“You can’t claim to be an important investment management or private equity player in financial technology if you’re not at the epicentre, which is London,” said Motive’s Rob Heyvaert. (Source: City AM)

What is certain is that London has always been a world-class city: popular, diverse, vibrant and successful. All our fundamental analysis says that the market is set for another sustained period of growth.

About Douglas & Gordon

- Douglas & Gordon was founded in Chelsea in 1958 and remains independently owned.

- The company employs over 200 people in 19 areas across Central, West, South West and North London, property services.

- Services include: Residential Sales, Lettings & Developments; Property Management; Corporate Services; Professional Valuations; Refurbishment & Interior Services, Asset Management; Block Management.

- £10bn residential property under management.

Our Data

The D&G Emerging Prime Index was established in 2014 using our proprietary data stretching back to December 2003.

The index is valuation based and covers the following areas of London: Battersea Park, Battersea, Balham, Clapham, East Putney, West Putney, Southfields & Earlsfield, Hammersmith, Shepherd’s Bush, Pimlico & Westminster and Fulham.