Market Report - Winter 2012 - 2013

Looking back to the beginning of 2012 at our predictions in terms of capital values, we are inclined to “cut and paste” what we said last year. The main driver for price increases for 2012 has been, as we stated last January, that “Prime Central London has become a magnet for capital from all over the world, particularly that part of the world that has seen most disruption in 2011.” Then we mentioned particularly the Arab Spring and the Euro crisis. Has anything changed? The Arab Spring is looking messy with progress towards stable democracy slow or stagnant, or even in reverse in Egypt, Libya and Tunisia. The Syrian conflict has escalated in the Middle-East, and the Israeli/Palestine peace process has gone into reverse. In geo-political terms you can add to this the change in leadership in China and the increasingly bellicose cries from Japan’s politicians in relation to territorial disputes with China and in the face of the nuclear threat of North Korea.

From an economic point of view, though the immediate crisis seems to have been averted in Europe, are we any clearer that there is the political will to back the creation of institutions that can effectively provide economic management? In the US, partisan political paralysis is presenting a major threat to the future of the world’s largest economy. World geo-politics therefore, based on top of a very restricted supply of property on the market as we enter 2013, leads us to believe that in D&G land as a whole we will be looking at price rises in the region of 8% over the next 12 months. We expect prices outside Prime Central London to rise more strongly as international buyers look beyond their normal hunting grounds.

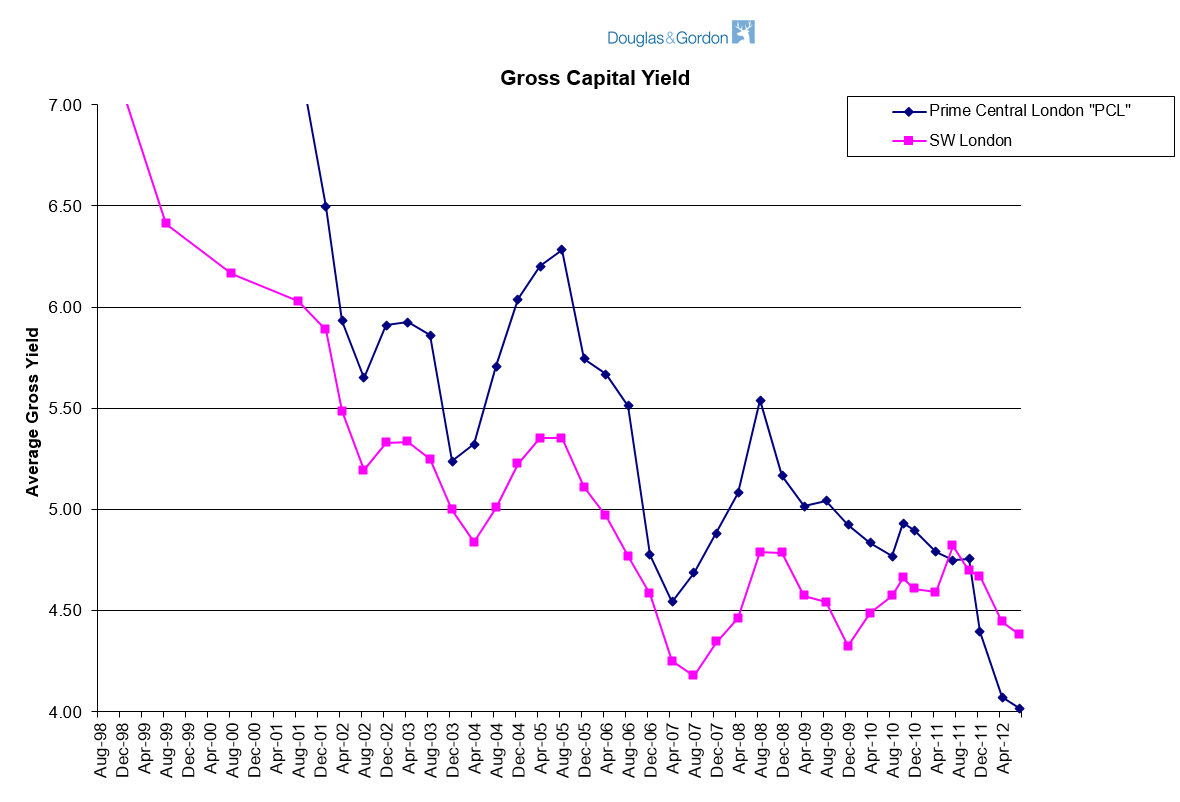

The outlook for the rental market in 2013 is not so positive. The top end of the market, “Prime” London, saw rents fall back at the end of 2012. There have been high profile redundancies in the City, and this has affected sentiment in the market. The London economy as a whole remains resilient and we have seen demand for property overall hold up. On the other hand, whilst twelve months ago we had only just recovered from a crisis in supply of property on the rental market, there has been a significant increase in property available throughout 2012. (More buy-to let?) Any economic recovery in 2013 will be led by London, so on that basis, we expect the decline in rental prices to stop and for rents to broadly stay flat.

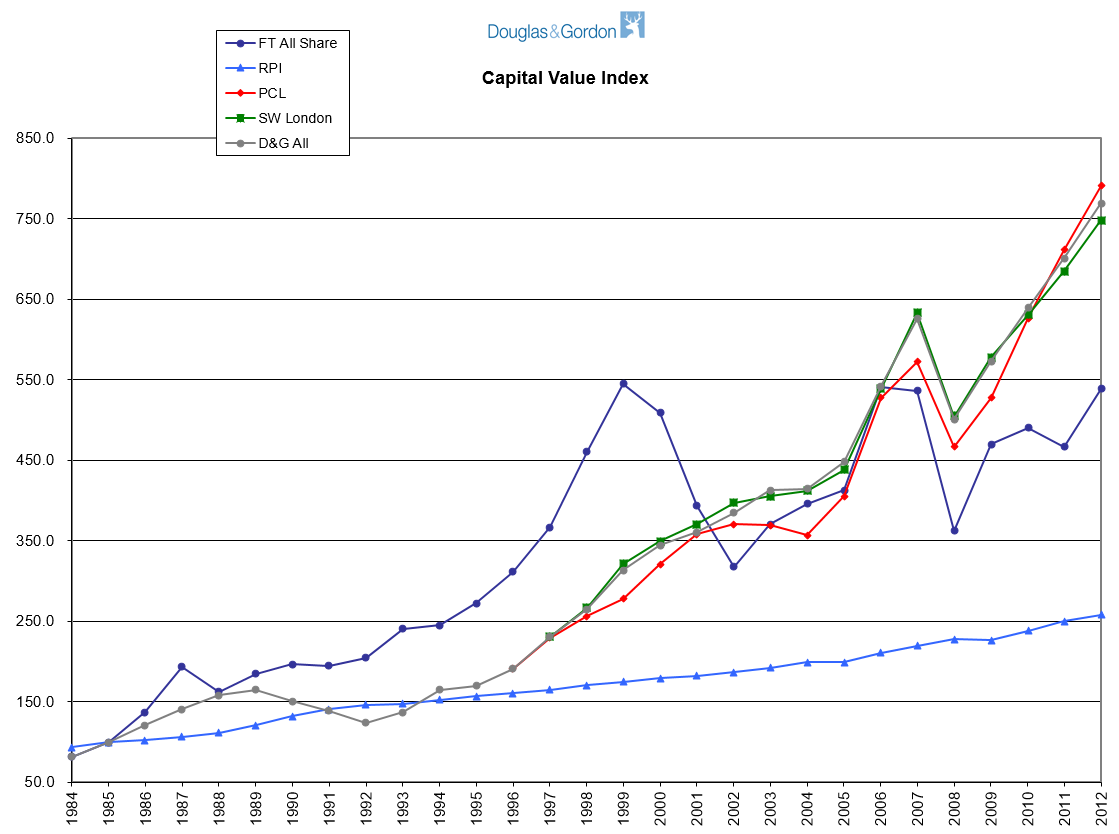

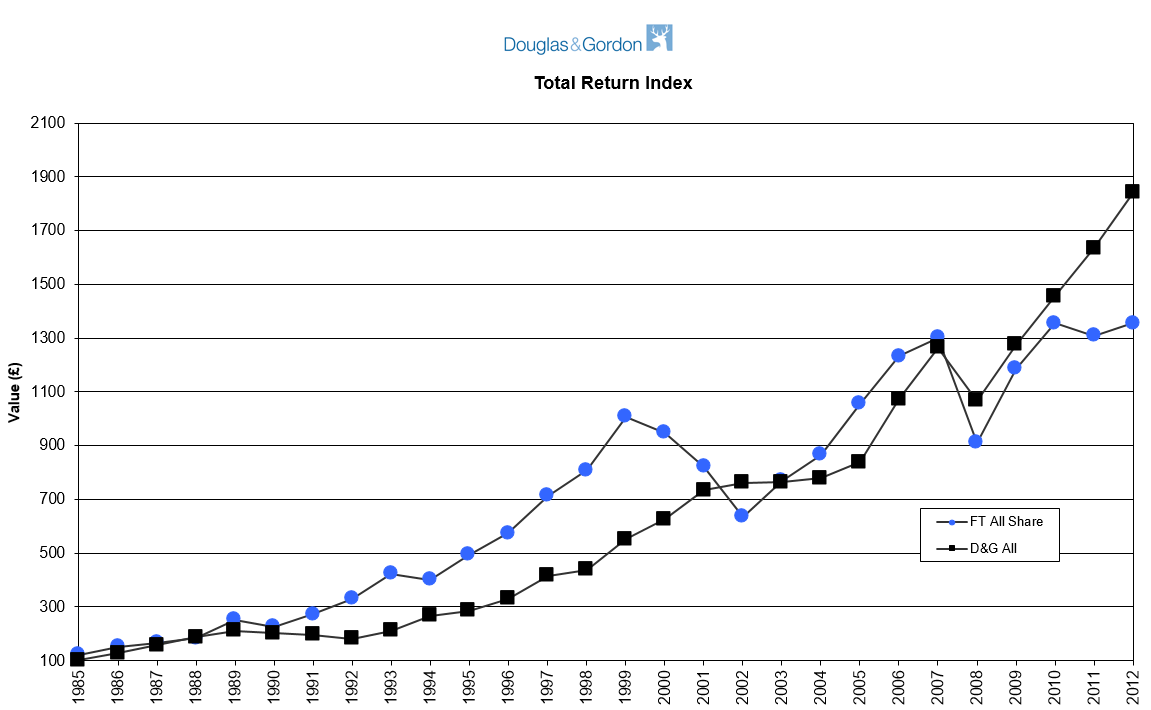

Reflecting on 2012, once again we come clean as to how our predictions of twelve months ago worked out. Twelve months ago we said that that “we do not anticipate the prices in PCL will move ahead quite as strongly as 2011, but do expect the increases to be in the 8-10% range” in D&G land. (Savills research predictions 3%, Knight Frank research 5%). The reality is that values moved ahead by 9.7% in 2012. Though the number of transactions has recovered from the lows of 2008/9, shortage of supply has kept activity at approximately 30% below peak levels. Regardless of the state of the Western economies, the emerging markets are still churning out millionaires and investment in London residential property has become a part of “normal “asset” allocation by the worlds high net worth individuals. We believe that such has been the pressure on “Prime” Central London from world demand that the peripheral areas such as Fulham, Hammersmith, and Battersea, Clapham, Wandsworth and Putney south of the river are attracting direct foreign investment. Whilst Prime capital values actually increased by 11.1% in 2012, the rest of D&G land saw increases of 9.3%, not far behind.

Our call of a 4% increase in rental values in 2012 was wrong. The outcome has been a negative 3.7% overall, mostly due to significant falls at the top-end of the market in the second half of the year. The sub £1000 a week market has more or less held its level through 2012. So in summary, supply was greater than we anticipated and demand did not pick up in line with a stagnant if not slightly declining UK economy.

Michael Hodgson