Market Report - Q4 2014

Market Report – Q4 2014

The fourth quarter of 2014 brought an end to 23 consecutive quarters of growth in the Central London residential sales market with a 2% fall in values. Before we consider whether this is just a blip – a breather to lower the market temperature from boiling to more of a simmer before it rolls on, or something more fundamental - how did the market perform during 2014 against our forecast of a year ago?

With regard to the sales market, last December we foresaw “growth being in single figures in the 5% to 7% range”. The outcome across Douglas & Gordon’s sixteen estate agency offices has been an average growth of 5.21% in 2014. For the second year running, the Emerging Prime market with growth of 6.52% has outperformed the Prime market where growth was 2.57%. In the rental market, we expected to see “supply and demand more finely balanced and therefore, only nominal rental growth of 1% or 2%”. Here, we were really quite wide of the mark with rents in D&G land overall increasing by 5.07% in the year. Again, there was stronger growth in Emerging Prime with rents increasing by 5.56% compared with by 2.15% in Prime.

What these annual growth rates hide is the fact that 2014 was very much a year of two halves. In both the sales and rental markets, the first six months showed strong growth – just under 10% in Emerging Prime and 3% in Prime for sales and over 2% in Prime and 4% in Emerging Prime for lettings. Thus, the market has been slowing since mid-year, so do we think this trend will continue in 2015?

The most significant single event in the calendar year 2014 for the housing market was the Chancellor’s unexpected reform of Stamp Duty in his December statement. Targeted to reduce Stamp Duty for the vast majority of transactions – 98% nationally – it has, on the one hand, given the green light to property transactions below the threshold (just under £1m), and on the other hand, piled additional expense on those buying and selling higher up the food chain. Given that the Labour party does not see the enhanced Stamp Duty even at a higher level, as a substitute for an annual Mansion Tax, we believe that the top end of the market will grind to a halt (even more so than it had already), in the first half of 2015 until after the General Election. We therefore see very differing outcomes in the sales market, depending on price bracket.

● In Prime London, we believe that properties up to £1m will increase in value in the 10%to 15% range, properties in the £1m to £3m range we think will increase by between 7% and 10% and those in the £3m to £5m range by 5%, maximum.

● In the Emerging Prime markets, we think sub £1m properties will increase by between 10% and 15% but in these areas, above £1m we believe that the additional Stamp Duty tax burden will curtail growth into the 0%-5% bracket.

● Against this backdrop of a fairly volatile sales market, we believe that the rental market will be steady but following the pattern of the second half of 2014, we see only nominal rental growth of 1% or 2%.

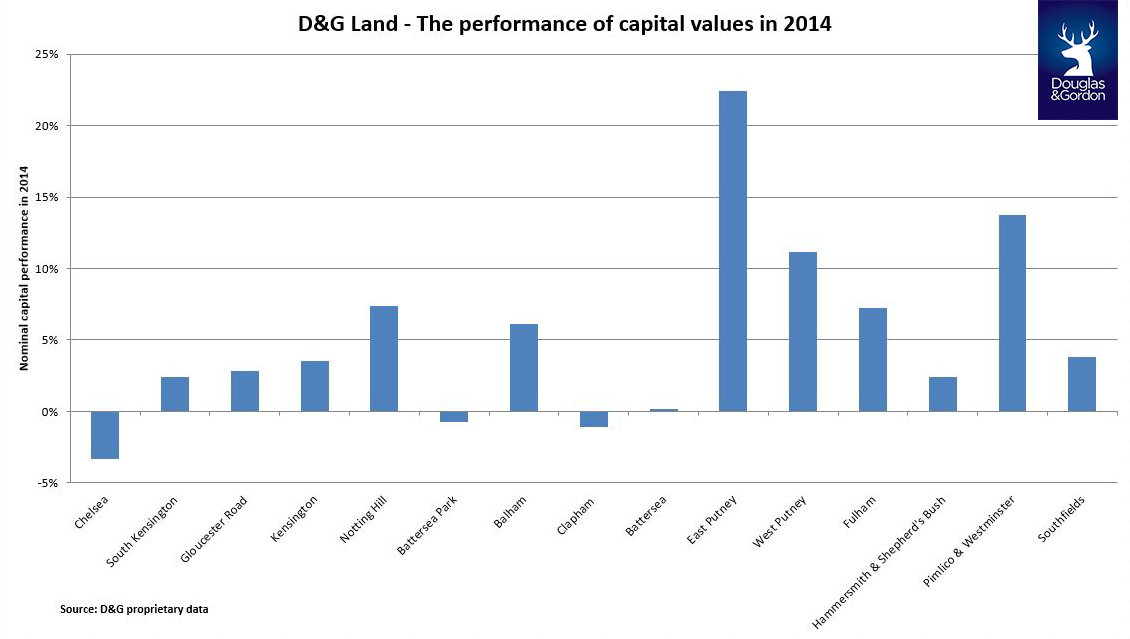

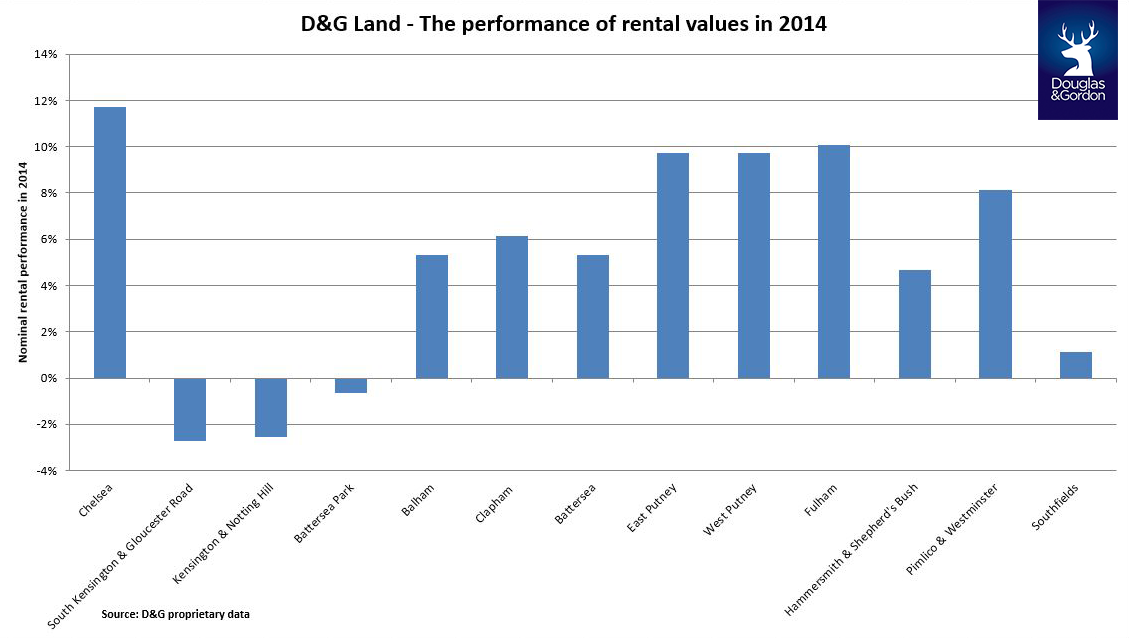

If you are an owner occupier or an investor in D&G land, what use is data regarding the area as a whole? As we have said in many of our reports over the years, every area is different and the bar chart below illustrates this graphically. Within these annual growth rates, differing types of property perform very differently. We will analyse these trends in our local area Investor Views Q1 2015 where we will analyse what happened in your market in 2014 and look forward to 2105. However, if you are impatient to know what your property is worth, contact your local Douglas & Gordon office.

Michael Hodgson

Chairman