Market Report - March 2014

Market Report – March 2014

“Price increases may be more modest for the rest of the year…..”

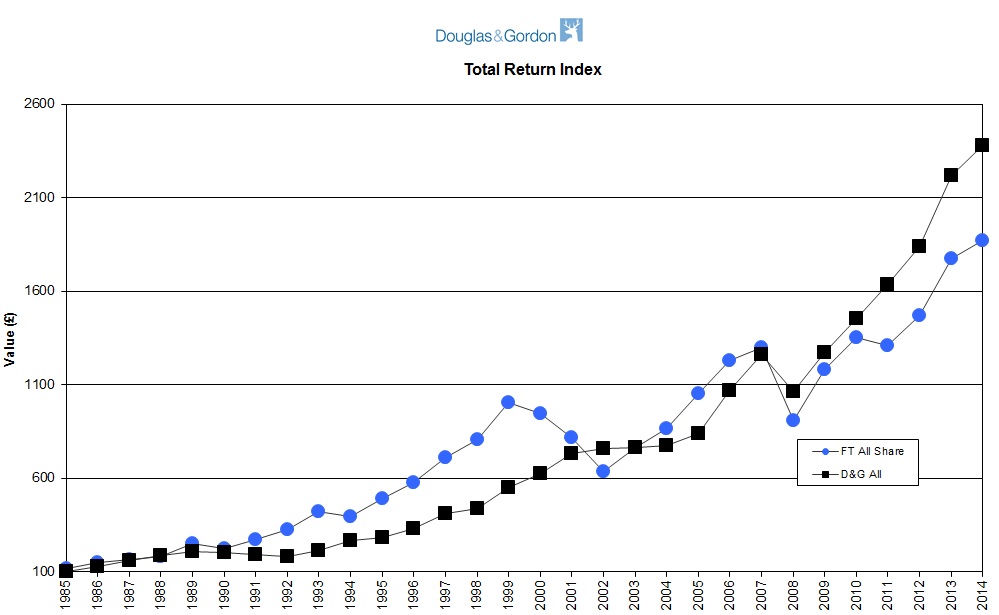

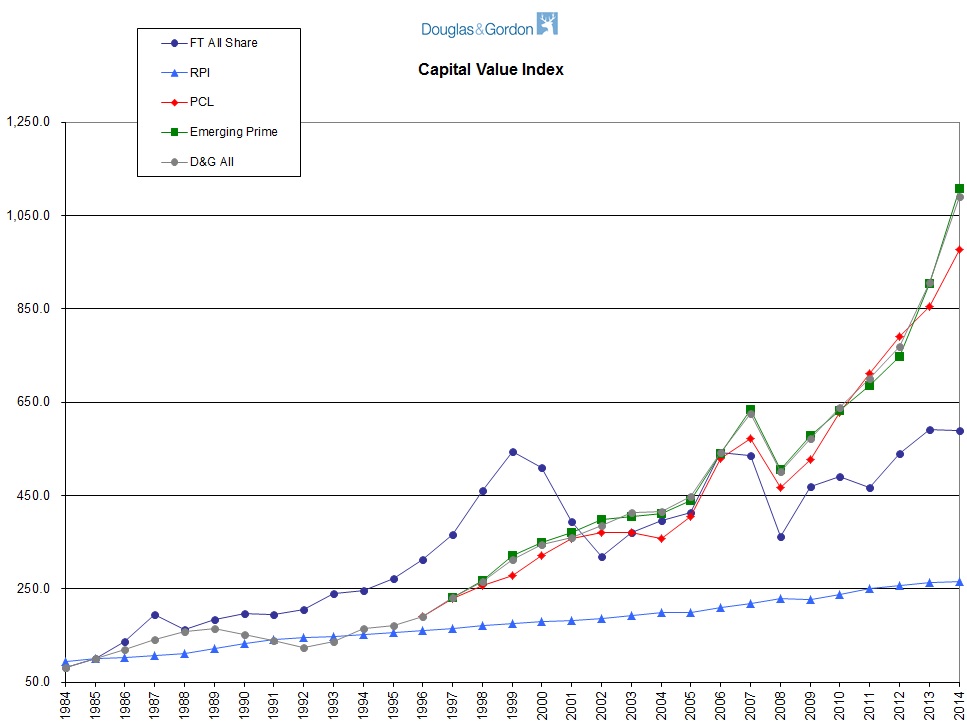

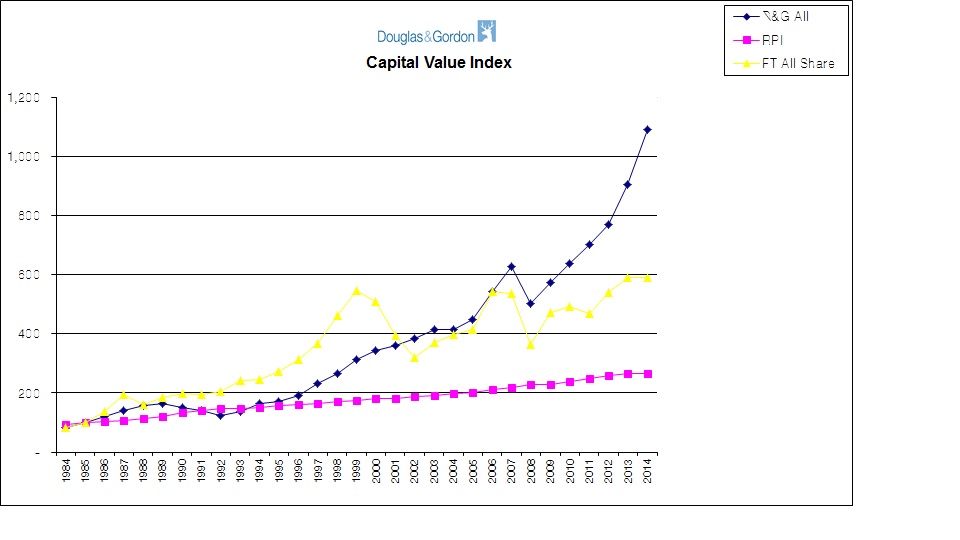

Land Registry figures recently published show that the value of properties sold in D&G land in 2013 hit £11.2 billion - a record and 30% up on the 2012 figure. The number of properties sold in the year was also up by 15.3% and the highest since 2007. The market therefore entered 2014 with considerable momentum behind it and once again, commentators’ predictions for the year as a whole are already looking modest, given the first quarter’s growth in values. Overall, in D&G land, prices moved ahead by 6.8%, taking the annual rate of increase to over 20% (20.4%). Overall, too, the rental market showed growth in the quarter, though at a comparatively modest 2%. There were, however, some variations in performance between the area we call Prime Central London and the periphery where we are going to replace the rather cumbersome “Non PCL” with “Emerging Prime”, as the area more and more takes on the characteristics of Prime.

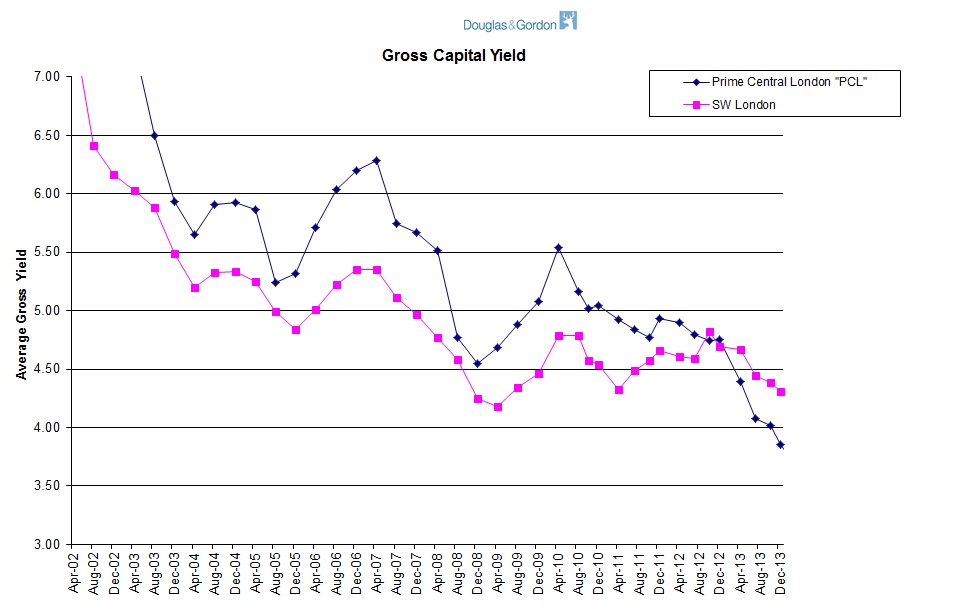

In Prime Central London, capital values moved ahead strongly in the quarter by an average of 7.1%, lifting the annual rate to 14.2%. The improvement in rents continues with a 2.1% on average increase during the quarter, taking the annual rate of increase to 7.3% - the highest rate of growth since 2011.

In the Emerging Prime area, capital growth has been strong, although not quite the same level as PCL, with a rise of 6.7% in the quarter, taking the annual rate up to 22.4%. Rental values added on average 1.9% but there has been no growth in this market over the last twelve months. In fact, a small decline of just under 1%.

Looking at the performance of different categories of property, it is interesting to note that in capital terms, the best performers have been one bedroom flats. In the Emerging Prime area, for instance, after a strong first quarter of 2014, annual growth hit 25.3%. There is a degree of catch up with one bedroom flats, made possible with greater availability of credit and perhaps, too in these more outlying areas, benefiting from the Government’s “Help to Buy” scheme. From a rental perspective and, therefore, from an investment point of view, one bedroom flats are simply easier to let.

Looking ahead, there are signs of a slight shift in the sales market with supply of property (from a very low point), up some 10% year on year and demand easing with a 7.8% reduction, year on year, in buyer registrations. This would suggest that price increases may be more modest for the rest of the year with in particular, international interest becoming more circumspect as the general election, fixed for May 2015, approaches. It is evident from our own experience that a significant factor behind the increase in supply of properties to sell is from the lettings market and this despite healthy capital value rises. We think Capital Gains tax changes are forcing some landlords’ hands. Supply to the lettings market is down 19% year on year though, with demand for rental property holding firm, it is likely that rents will continue to rise throughout the rest of 2014.

Michael Hodgson