Market Report December 2013

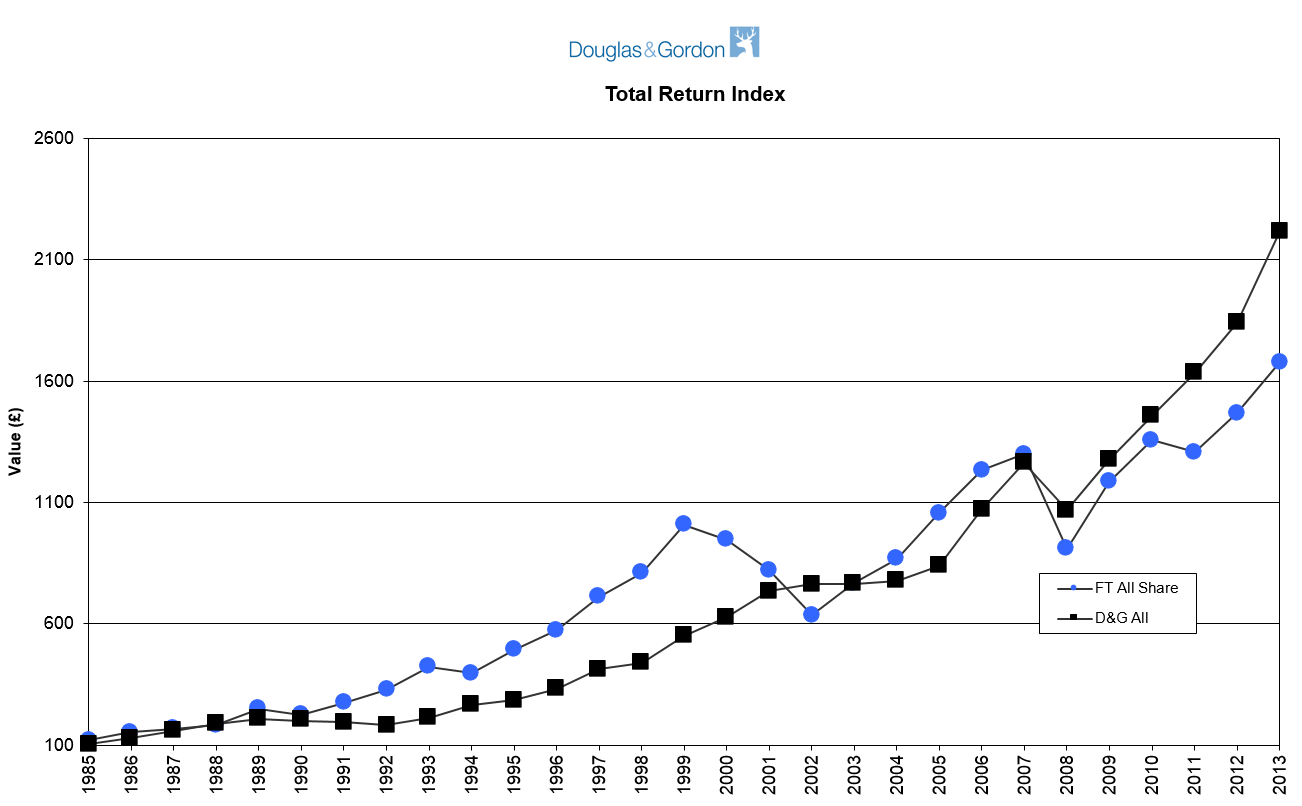

The value of properties sold in D&G land in 2013 is heading towards £10.5 billion – a more than 20% increase on the figure for 2012 which was itself a record. In terms of numbers, more than 11,000 have been sold in the year – an increase of nearly 10% over 2012 and the highest volume of sales since the peak year of 2007 (13,000 sold). What this shows is that the reality behind the apparent lack of stock, according to many agents, is that properties, faced with very strong demand, have simply sold very quickly.

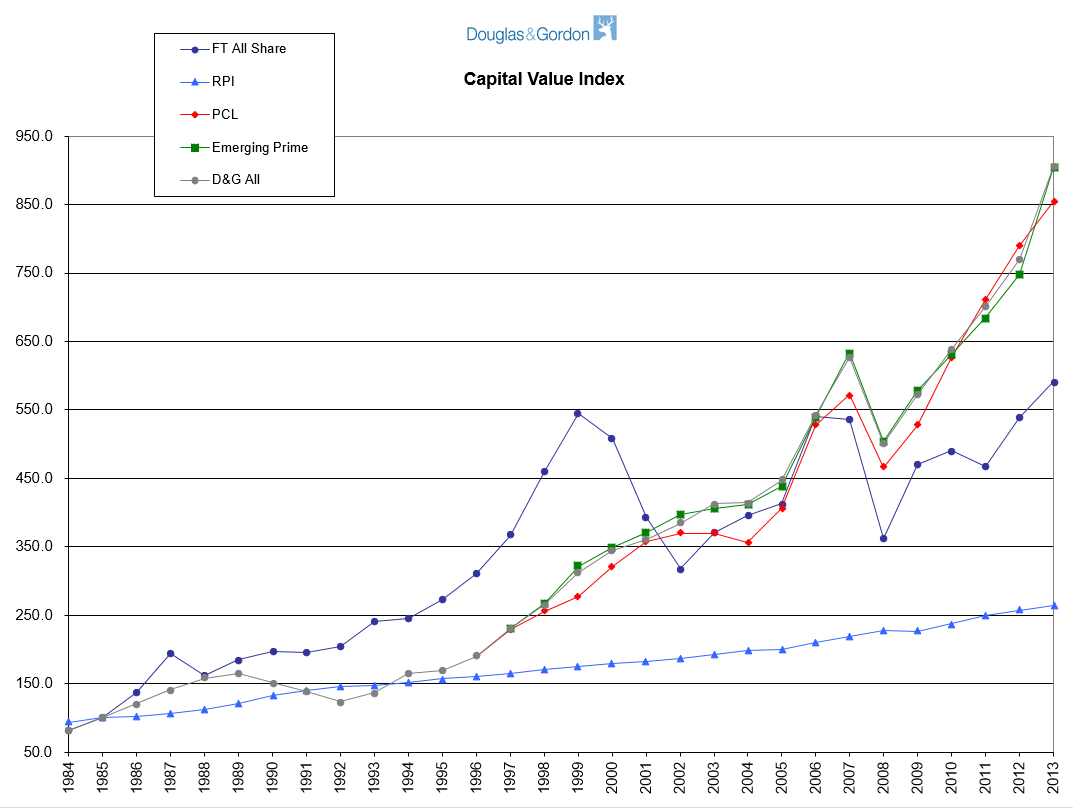

With the year behind us and unlike some of our more resourced competitors, we face up to the forecasts we made twelve months ago for the central London sales market. Unlike in 2012, when the sales market moved ahead 9.7% against our forecast of within the range of 8% to 10%, in 2013, our forecast of 8% looks very undercooked against an astonishing final result of an increase in sales values of 17%. In mitigation, we were spot on in Prime Central London where values moved ahead by 8.2%. The most extraordinary feature of the market in 2013 was the increase in values of property in the “rim” around Prime Central where values increased in the year by nearly 21%. After a couple of years of just lagging PCL, “Emerging Prime”, as we are going to call the rest of D&G land (previously variously named “non-PCL” or “SW London”), as on Capital Value Index graph, has surged ahead in the last twelve months. Our analysis behind this suggests that it is not just the ripple effect i.e. owners of PCL selling up and reinvesting in non-PCL but in addition, that the international market has now discovered non-PCL and deduced that there is better value over there. Russians are buying in Kennington and Kensington!

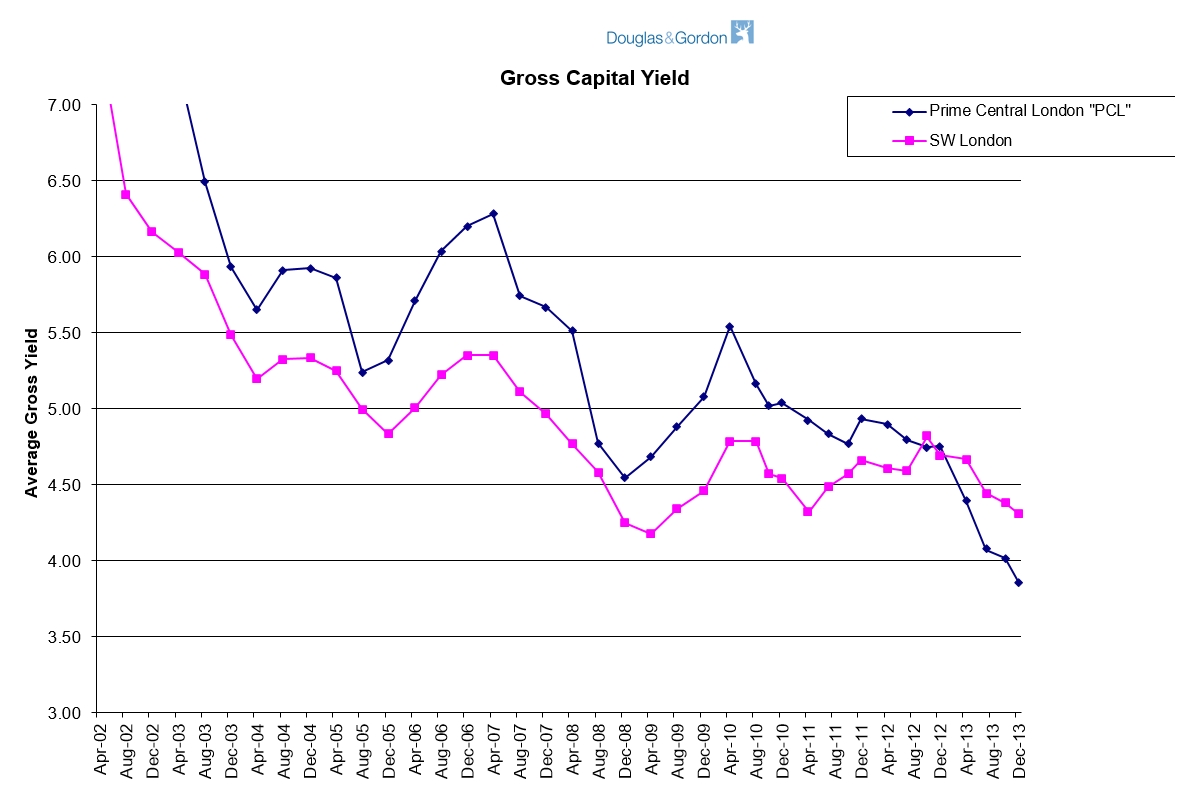

On the rental side, our forecasts fared a little better. Overall, we thought that rents would be flat. In Prime Central London, for the first time for three years, there was rental growth, albeit very marginal, at less than 1%. But outside this area, quite possibly as a result of significant investment purchase, supply continued to outrun demand and rents fell, on average, by just under 4%.

Undaunted, we are going to forecast for 2014 that sales values will continue to increase. Worldwide demand for London residential property as a “safe haven” is sure to continue but it may be tempered by the approach of the general election in 2015 and politicians’ cries for mansion tax and the like. We therefore see growth being in single figures in the 5% to 7% range. In the rental market which is more related to the performance of the London economy, we see supply and demand more finely balanced and therefore, only nominal rental growth of 1% or 2%.

Michael Hodgson