Growth slows but it’s still growth - Market Report July 2012

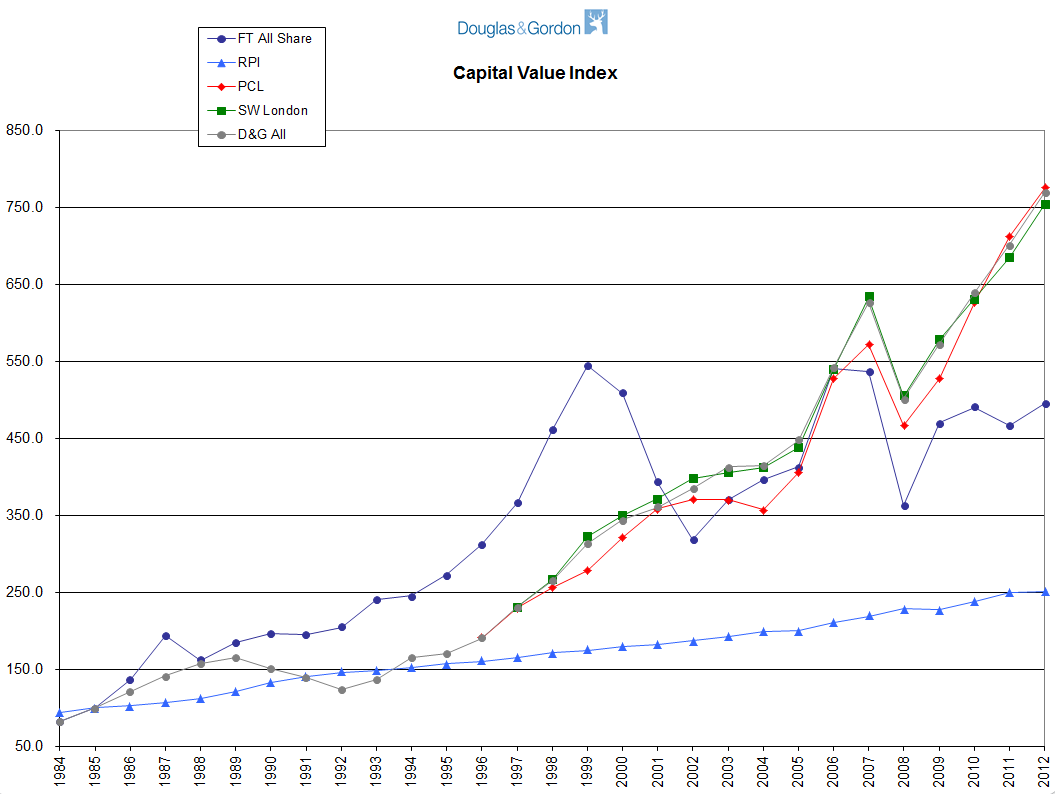

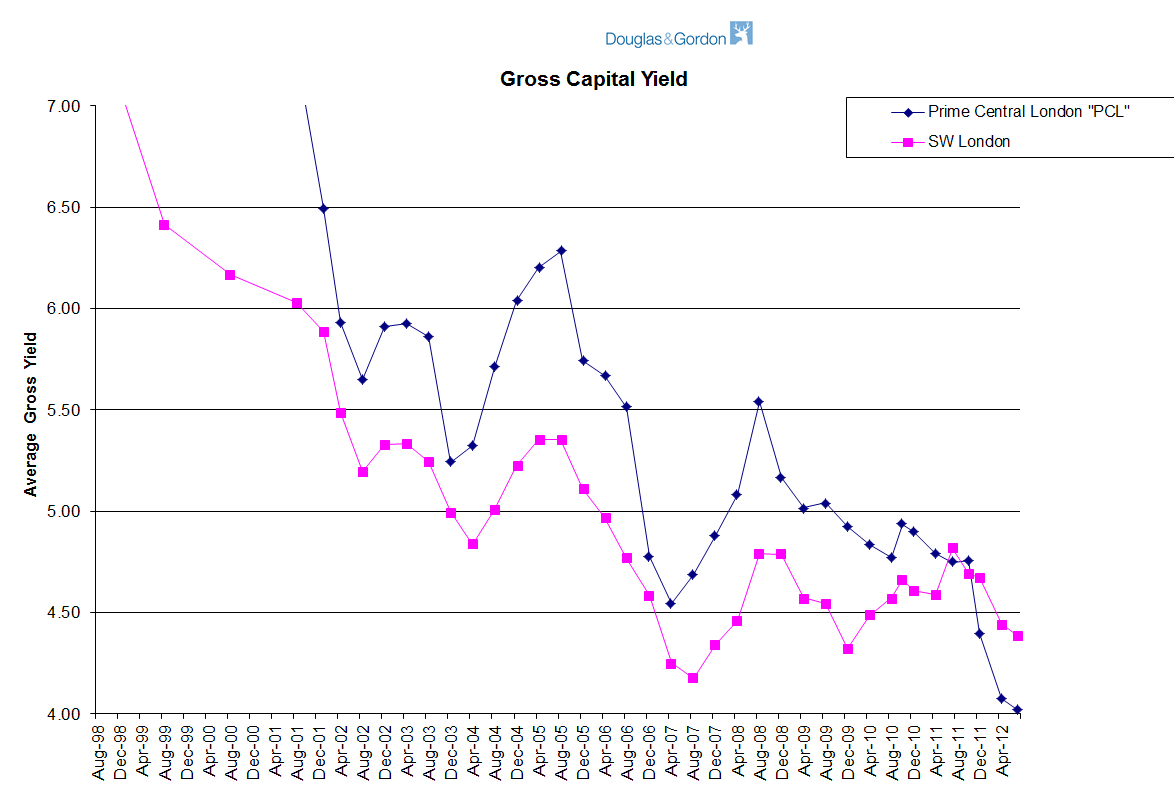

In the quarter to June 2012, sales prices increased in D&G land overall by 1.7% with Prime Central London (Chelsea, Kensington & Notting Hill), slightly underperforming with an increase of 1.2% and the rest of D&G land ( South West London (“SWL”)) moving ahead by 1.9%. Year on year, PCL has increased by 8.8%, SWL by 10% (see Capital Value Index).

London continues to draw in buyers from all over the world and the number of buyer applications in the quarter was within 1% of the equivalent period in 2011. However, supply is up, reducing the applicants per property ratio from 5.8 down to 4.4. The escalating Euro crisis, Jubilee celebrations and Olympic Games preparations are all factors which affect sentiment and volumes. Whilst only a quarter has passed since the Budget and the controversial stamp duty revisions announced by the Chancellor, the stand out statistic is the only sector of the market to have actually experienced a negative in the quarter is houses over £2m in Prime Central London. On the other side of the coin, family houses below £2m have seen the greatest increase – 2.3% in the quarter. That’s what happens when you introduce an arbitrary threshold!

The rental market is essentially flat with a 0.1% increase in the quarter to June 2012. Although the latest quarter follows two quarters with overall (very slight), reduction in rental values, there has been a 20% increase year on year in the number of properties available to set against only a 10% increase in the number of tenant applications. Landlords will therefore need to be realistic in their aspirations for rental levels during the busy summer market, the operation of which will be complicated by the Olympic and Paralympic Games in August and September.

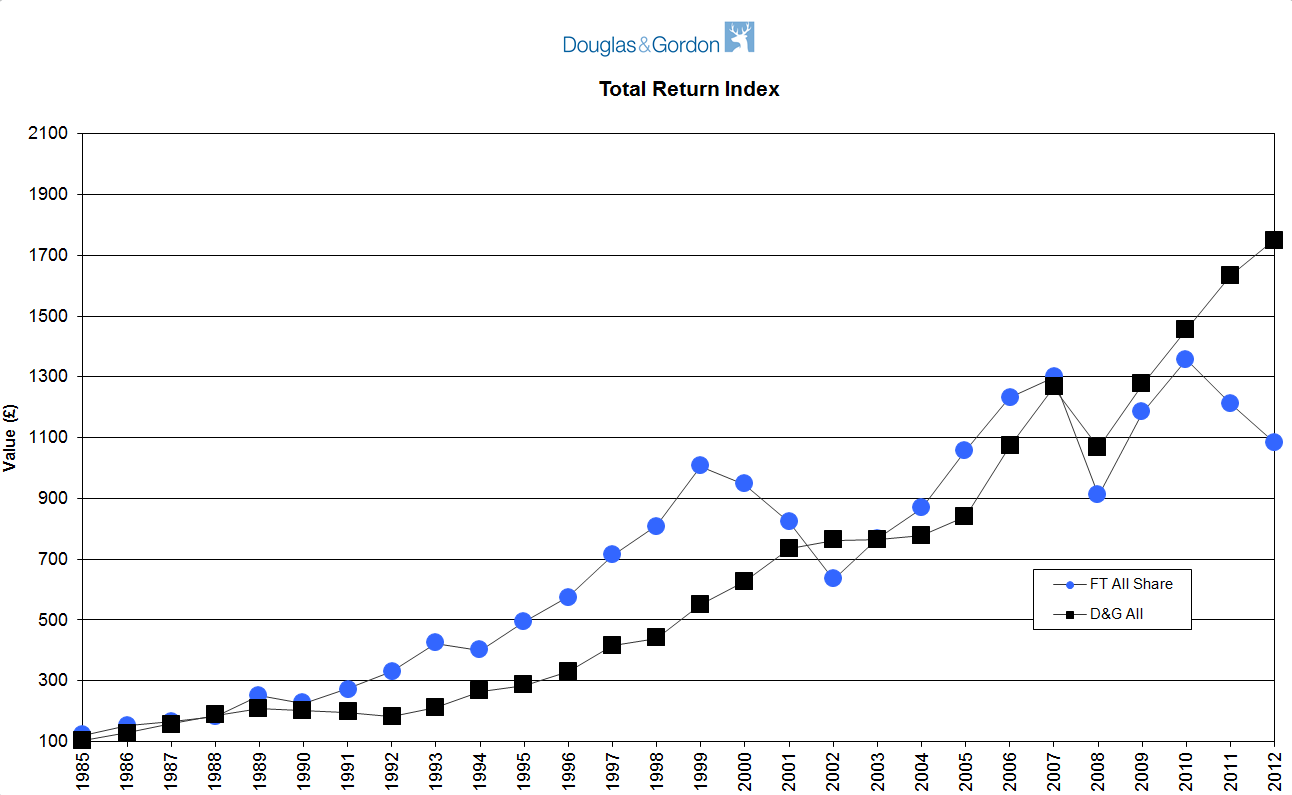

The gulf in performance, in investment terms, between Central London property and the FTSE All Share is greater than it has ever been (See Total Return Index). Can this carry on? As the rest of the world gets more unstable – Euro crisis, the Arab Spring, a changing of the guard in China – London will draw in more capital. But against that trend, our politicians are grappling with immigration worries, a desperate need to raise revenue with “rich” foreigners an obvious target and a series of regulatory issues surrounding the City, a major force in the UK economy. How they deal with these will influence investment decisions in London.

Noting that London subsidises the rest of the UK to the tune of £15 billion each year, the Economist (June 30th “London on a high”), sounds a warning – “London’s prosperity is built on its ability to attract the rich, the clever and the hard-working from all over the world. Anything that jeopardises the city’s internationalism endangers its future and anything that jeopardises London endangers the country”

Michael Hodgson