Market Report 1st Quarter 2013 Chelsea Kensington South Kensington Notting Hill

Chelsea - Kensington

South Kensington - Notting Hill

“We analyse the absolute performance of residential property in each of the 14 London areas covered by Douglas & Gordon. We also examine the relative performance, comparing different unit sizes and different areas. Finally, in a city that attracts global investors, we try to place residential property performance in a wider macro-economic context.”

What Drives Prime Central London (PCL) prices and what is the outlook?

Close and well-established relationship between the rise in wealth of global High Net Worths and capital values of PCL. Source: Capgemini, Merrill Lynch, D&GAM.

PCL is an asset backed play on the rise of wealth in emerging market economies (London “capital of the BRICS” – Jim O’ Neil, Chairman of Goldman Sachs Asset Management).

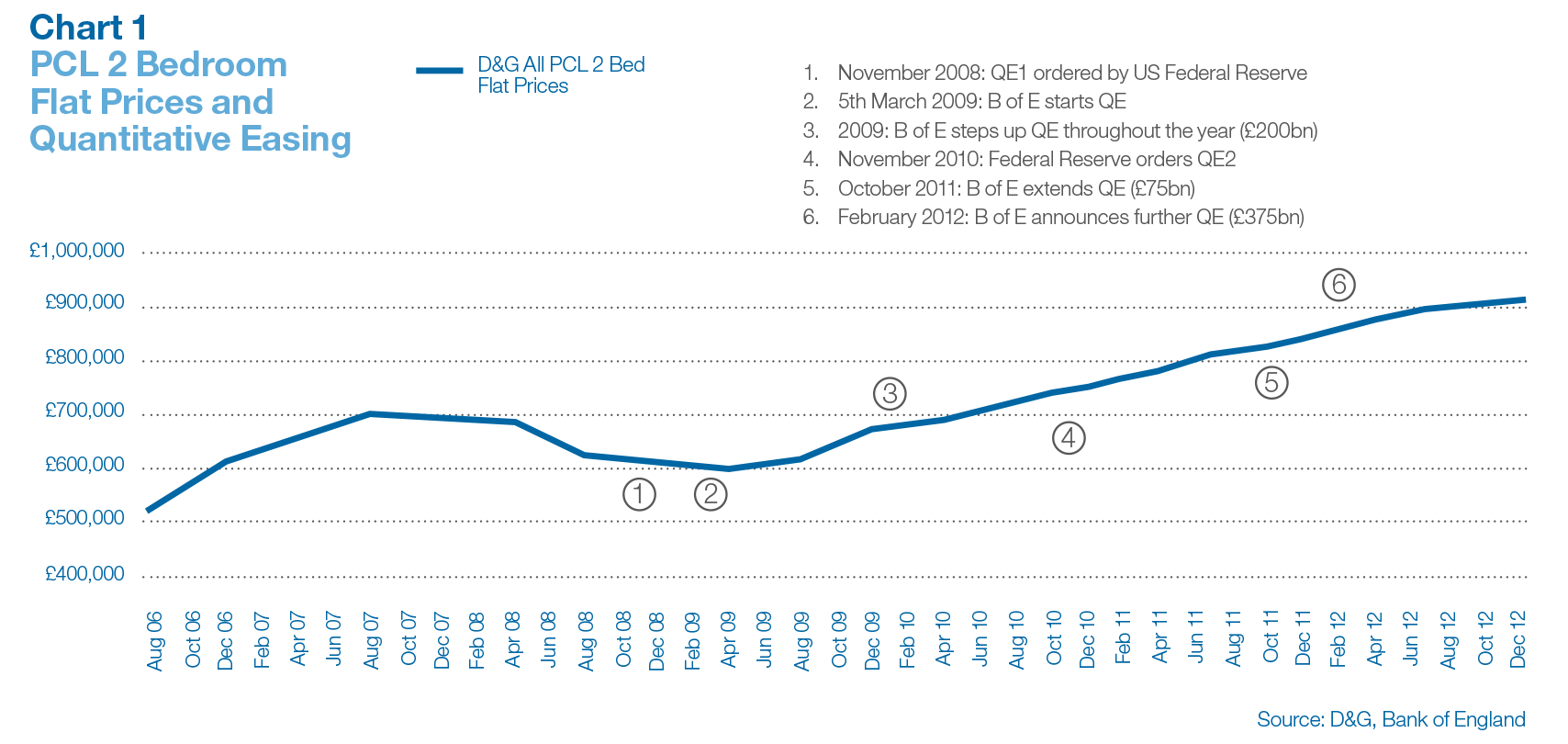

Chart 1

One of the stated effects of QE is to raise asset prices in order to boost consumer confidence.

House prices are a powerful transmission mechanism of monetary policy to consumer confidence.

In the USA QE has successfully boosted average house (and other asset) prices. The Bank of England, under a new governor, will want to do the same, via QE, for average UK house prices.

However QE has a Bunsen burner effect on house prices. Prime assets are nearer the QE flame and move quicker and further than average assets.

2013 PCL Forecast

D&GAM has, for 7 years, been the investment adviser to a fund that invests only in PCL (The Prime London Capital Fund).

We agree with the Manager of that fund when he says in his latest quarterly report:

“QE is all about making the UK consumer more confident and to do that the average UK house price needs to rise. If QE is used by the new governor to raise average UK house prices then one sure side effect, and prelude, will be a much higher percentage rise in prime risk assets,like PCL.” Source: www.primelondoncapitalfund.com

UK monetary policy (interest rates and level of sterling) is set to stay loose for the next few years and in this environment we think that capital values in PCL will continue to rise.

Forecast for PCL in 2013:

– 10% up in £ terms

– Flat, or even down, in US$ or euro terms

How to tell if/when PCL is over-bought...

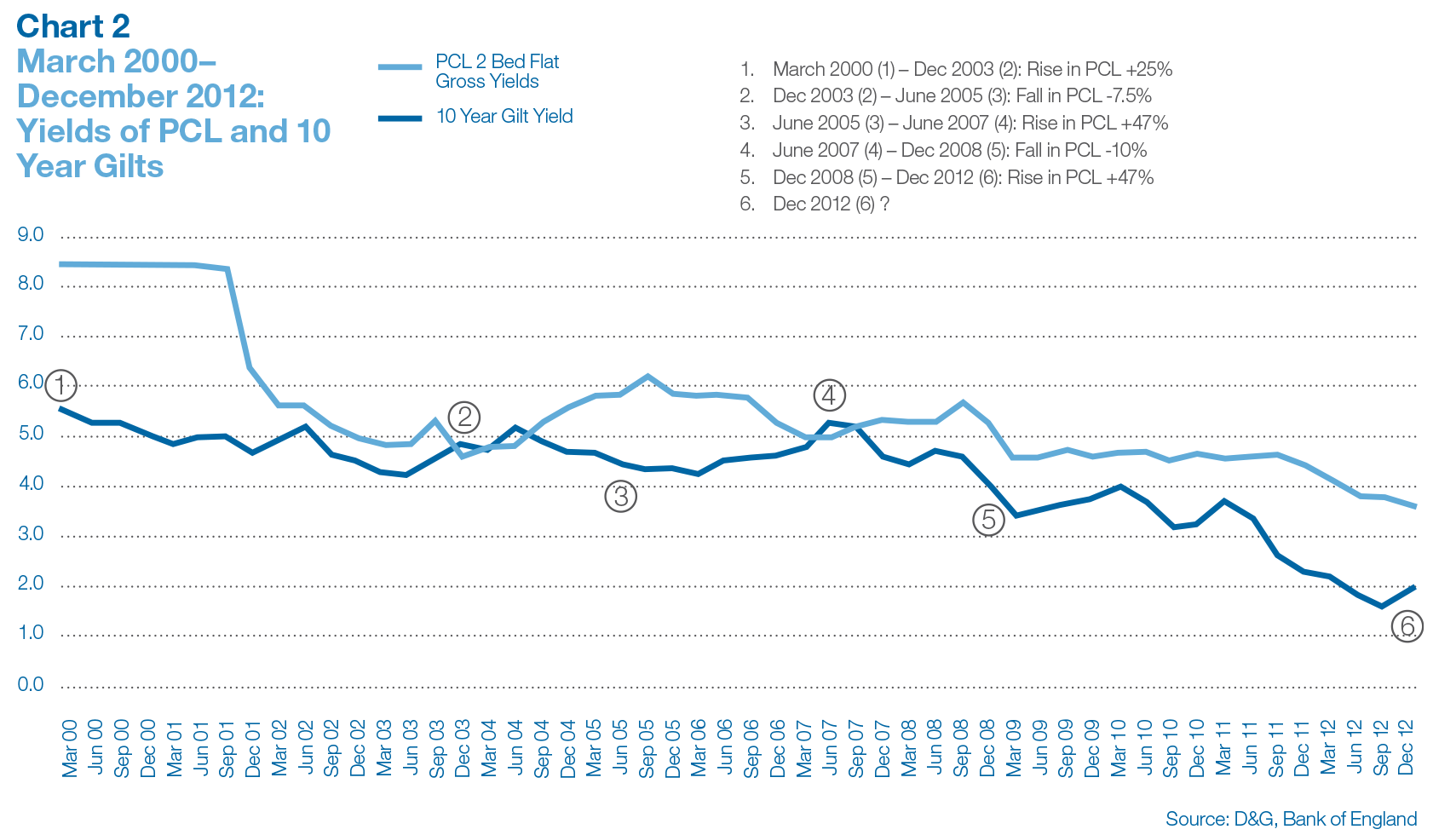

Chart 2

One of the most useful guides to PCL future capital values has been the relationship between gross rental yields on PCL and 10 year Gilts (UK Government Bonds).

When the yield on 10 year Gilts is above the equivalent gross PCL yield, PCL capital values have fallen (see points 2 and 4 on Chart 2).

This is a classic reaction to risk-free returns being higher than “risk assets.”

When the opposite is true and the yield on 10 year Gilts is below the gross yield on PCL,capital values have risen (see points 1, 3 and 5on Chart 2).

The gap between the two yields has also acted as a guide to the likely speed and direction of PCL capital values.

Over the 12 year period covered, gross yields on PCL have been on average 35% higher than on 10 year Gilts. The gap is currently 85% suggesting that PCL capital values still have further to rise.

Conclusion

The debate about the level of PCL prices is hardly new. Pepys, in his 17th century diaries, complains how expensive Whitehall has become. Domestic owners and commentators often underestimate the reason why PCL properties are sought by buyers from all over the world. The sanctity of contract and title, the rule of law, transparency and liquidity of the London market are all factors that override cyclical economic or financial changes. The irony is that it is Londoners, trying to catch the “top”, who sell and then regret. Whereas overseas owners, who know “less” hold PCL for the long-term and benefit.

And finally…

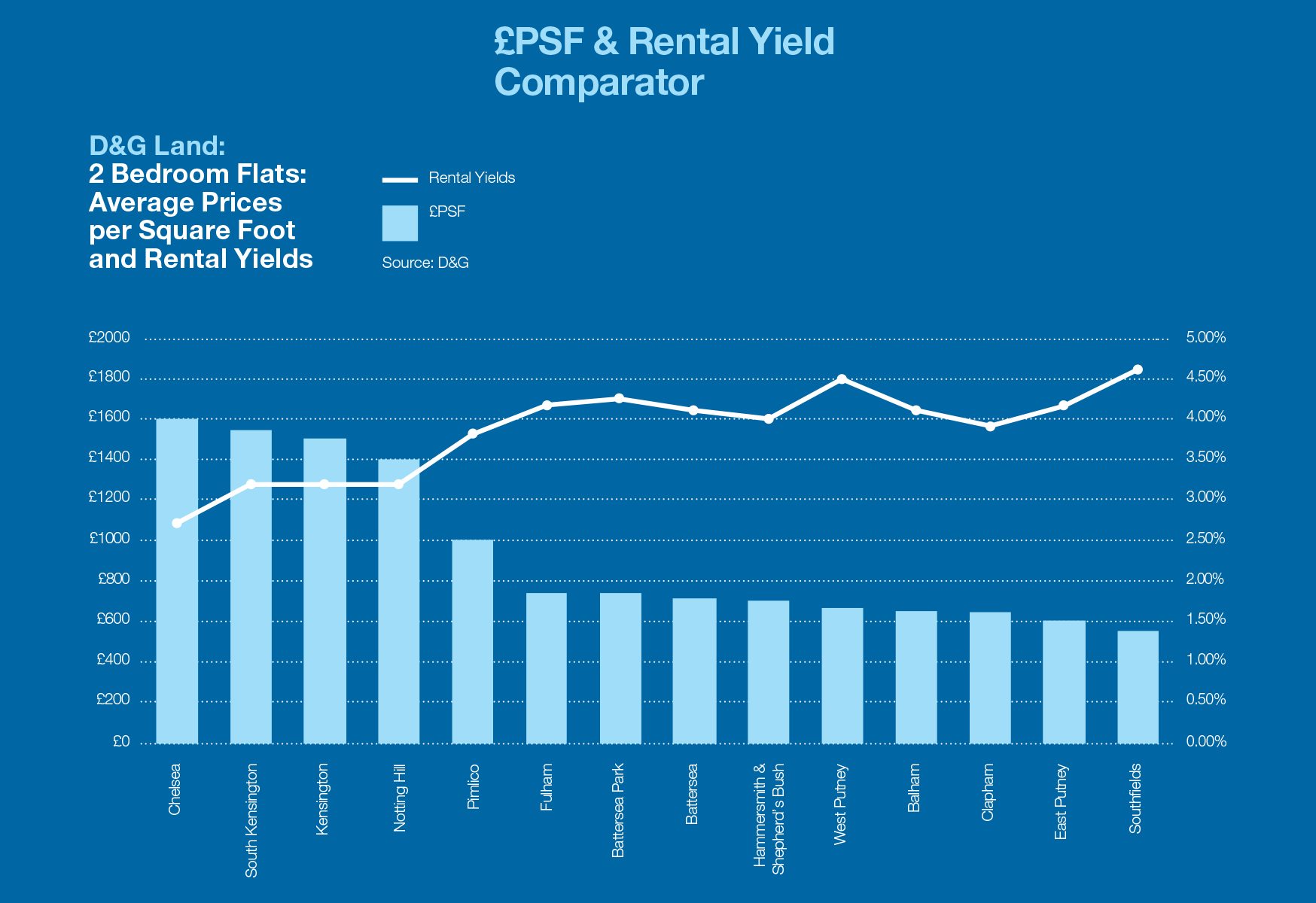

D&G Research covers all 14 of the London areas where Douglas & Gordon has an office, a full sales and lettings team and long-standing, proprietary and reliable data. The chart (above) gives an idea of the relative position of the different areas from the perspective of average PSF and rental yields. If you would like to read research on other D&G areas, or talk to either our research team or a negotiator in one of the offices, please contact Andrew Monteath, Head of Research D&GAM on info@dngam.com

Key Contacts

Ed Mead

Sales Director

+44 (0)20 7225 1225

emead@dng.co.uk

Nicky Chambers

Lettings Associate Director

+44 (0)20 7581 6666

nchambers@dng.co.uk