Market Report – September 2011

Since our last Market Report (July 2011), all hell has broken out in the financial markets in the UK and worldwide. Of course, that raises questions as to what impact do the financial markets have on the Central London property market? As stock markets fall, do property owners think that the value of their houses and flats will follow and sell now, hoping to buy back later at a lower price? On the other hand, do they view property as a more stable investment than the stock market and a safer place to leave their wealth? In the very short term – the last quarter – indications are that vendors are taking the latter view. Year on year, volume of property for sale is down by 11% so as yet, there is no rush for the gates.

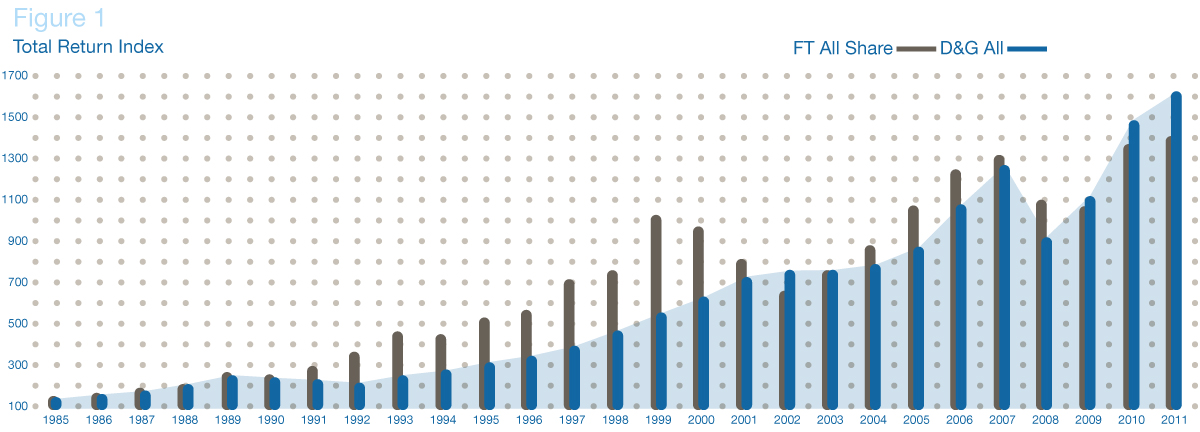

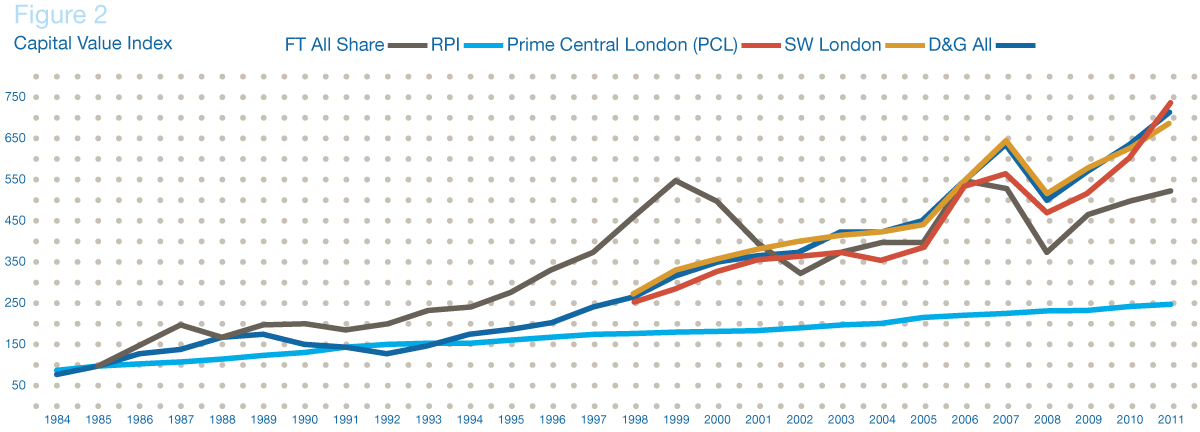

With shortage of supply still the dominant factor in the Central London market, prices continued to rise in the third quarter of 2011 with an overall average increase of 2.5% in D&G land. In our July report, we observed that increases in Prime Central London in the second quarter of the year outstripped those in the immediate surrounding area. In the third quarter, this trend was reversed with the outlying areas seeing a just over 3% increase and Prime just 1%, confirming the not so surprising finding that these markets are very closely linked. The same can be said for the lettings market where overall, 0.6% in the quarter split just over 1% in PCL and 0.25% on PCL’s periphery. Nevertheless, the performance of Prime Central London over the last two years has outstripped that of the adjoining areas (see Capital Value Index graph X), in terms of both capital and rental growth. On average, capital values in PCL have increased by 38.9% in the two years to October and rental values by 31.7% over the same period. Growth in the adjoining areas has been capital 22.4% and rental 25%.

What will the final quarter of the year bring? In our July report, we “predicted that (in the second half of the year), prices will rise another 4% to bring the annual total to 10% and some types of property have already exceeded that in the first six months of the year”. The rise in the third quarter has taken the annual increase to about 9.5% and our feeling is that after two years of steady – and some spectacular – quarterly increases, the market may be cooling down a bit to prove our July prediction for the year about right. We still believe, however, that there is potential upside to growth and very little downside, given the paucity of supply in relation to the demand for properties both for sale and to let. In the lettings market, although the supply of property is up year on year by 11%, this extra supply is dwarfed by a 26% increase year on year of potential tenants – a product of continuing difficulties in raising finance for purchase and job uncertainty.

Michael Hodgson